Am I part of the luckiest generation in history?

42 minutes ago

Evan DavisPresenter on Radio 4’s PM

Evan DavisPresenter on Radio 4’s PM

Getty Images

Getty ImagesI was born in 1962, at the tail end of the baby boom era.

Does that make me especially lucky? Should I languish in guilt?

The claim has been made that the baby boomers in general, and the late baby boomers in particular, have done rather better than the generations that followed.

This argument has been bubbling for some years, but my interest was piqued by comments from the former foreign secretary William Hague, now chancellor of the University of Oxford – born in 1961 – who argued a few months ago that the early 1960s is one of the best periods in history in which to have been born.

And recent arguments over the English student loan system have put generational fairness even more firmly onto the agenda.

When I was young, I don’t remember fairness between generations ever being given much thought, and the labelling of different cohorts (Generation X, millennials, Gen Z and Gen Alpha) wasn’t quite the thing it is now. The baby boom was talked about, but more as a simple demographic phenomenon. Now, generational analysis seems to be everywhere; from TV comedies like Hacks and Only Murders in the Building, to office-place chitchat.

But with generational identity politics alive and well today, let us examine the evidence. I find Hague’s claim fascinating and plausible. But is it right? Have my schoolmates and I done well – too well? I can’t cover everything, so I’ll focus on England, and three key areas: higher education, pensions and housing.

The ambiguous student loan issue

There’s clearly a sense of injustice about the English student loan system.

Martin Lewis, Britain’s most prominent financial commentator, has criticised the terms attached to some of the loans as immoral.

Indeed, the extra 9% “tax” on earnings paid by younger graduates is an obvious difference to the treatment I received. In my case, the government actually gave me an annual maintenance grant and covered the cost of tuition.

Younger graduates feel this sharply. Natalie Whittaker, 27, told the BBC recently that debt from her bachelor’s degree now stands at £75,500 (up from £52,000 when she graduated). “We were told… it’s just the price of a coffee, you won’t even notice it leaving your pay cheque,” she says. But now she’s making repayments and thinking, “hang on a minute, this isn’t the price of a coffee”.

There are also suggestions that the state might actually be making a profit from graduates; recent work by the consultancy London Economics finds that the 2022 cohort of graduates will pay more into the exchequer through the loan system, over their lifetimes, than their degrees actually cost.

Getty Images

Getty ImagesBut I wouldn’t read too much into the overall profit the government is allegedly making (at a different time, the Institute for Fiscal Studies came up with the opposite result to London Economics).

In fact, the student loans issue is much more ambiguous than often realised, because while today’s students do pay far more than I did, a lot more of them have the chance to go to university.

To quote the House of Commons Library, “overall participation in higher education increased from 3.4% in 1950, to 8.4% in 1970, 19.3% in 1990 and 33% in 2000”.

And then, by 2022/23, 49% of state school pupils from England had started higher education by the age of 25. What was once a privilege for a few has become an entitlement for half of young adults.

So in this case, the victims of injustice are arguably not the students choosing to take out a loan and pay for college now, but the many people I went to school with who were never even offered a choice about whether to borrow and study at all.

The English student loan system might look unfair, but has been designed precisely to make the growth of graduate numbers possible, while also being fair to the declining proportion of non-students. In other words, the loan system aims to provide for fairness between generations, not fairness across generations.

Getty Images

Getty ImagesThere is one other very important feature of the student loan system though, which has angered some students. While it was not designed to be a big money-maker for the government overall, it is designed to make money out of some better-off graduates to cover the cost of subsidising some of the less well-off.

This comes down to the fact that it isn’t a true loan like a mortgage which you have to pay back over time regardless of your means. Instead, it is more like a personalised tax. And many will never earn enough to pay back the full cost of their higher education. The system is designed to cover the losses on those lower income graduates, from the profits made from higher income graduates. (Though, interestingly, the very-rich graduates have been penalised less than the quite-rich, because they can pay off their loan quickly and avoid paying the high interest rates.)

So if you made it to university in the 1980s, you would have been much better off then than now. In my years, students were subsidised. Now, the “top” students subsidise others. Even if my generation overall was not particularly lucky when it came to higher education, those of us who did go to university really were the most spoiled of all.

Lucky London buyers

I’m embarrassed to say there is a similar case to be made about housing. By buying a flat in London in 1988, I’ve arguably enjoyed an unearned advantage.

As it happens, I lost money on that flat when I sold it in 1995, but still upgraded to a bigger flat which soared in value over the two decades I held it.

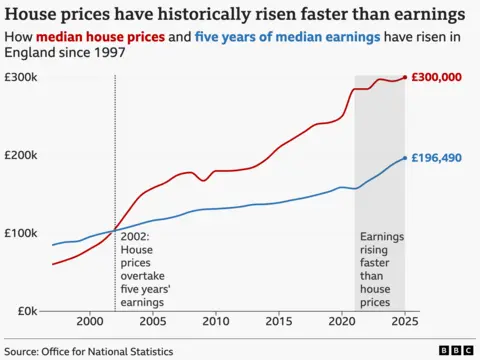

And that tells you the basic story of house prices in England which rose relative to earnings from the early 90s to 2021. If you managed to buy a property before the mid 90s – as many of the boomers did – you’ve likely enjoyed substantial capital gains. If you came into house-buying age after 2015, you’d already drawn the short straw.

Lauren Finch, who earns a £24,000 annual salary at a GP surgery, told the BBC last year that it was “soul destroying” to still live with her parents aged 29, adding that she often house-sits for friends just to get a sense of freedom.

Interest rates complicate things slightly. Globally, in recent decades, interest rates have fallen very significantly, providing a huge gift to younger buyers who can now borrow at much more favourable rates than I could when I first bought. Few house-buyers would like to revisit the world of the 15% I remember paying on my first mortgage.

But there are only so many houses. The fact that it’s cheaper to borrow means the price of houses has to go up, to ration the available supply. The gift of low interest rates comes with the burden of high house prices.

The timing was propitious for those who bought as this transition from a high interest rate regime was occurring. I was lucky in that regard, as were many of my cohort.

That all being said, there has been something else going on in the UK housing market which means that even among those born in the baby boom years, there is a big degree of inequality.

London and its catchment area have enjoyed bigger gains than elsewhere. When I left university in the mid-80s, London had been seen as a city in decline. The population had been falling for years; the words “inner city” were regarded as a mark of degradation. But then by 2000, London had found its mojo and had become a global hub again. And property prices reflected that.

XNY/Star Max/GC Images

XNY/Star Max/GC ImagesAnd add to that, London’s adult population between 1996 and 2021 grew by 29%, while the number of homes only grew by 23%. No wonder it’s hard to buy or rent in the capital. In the rest of England, the number of dwellings and the population has grown in a much more balanced way.

It means that if you were lucky enough to buy in London, you were much more of a winner than home-buyers elsewhere in the country.

Gold-plated pensions

Finally, we need to look at pensions, where I think it is fair to say the baby boom generation have looked after themselves rather well. They are enjoying the benefit of pensions paid for by today’s working population, which are notably more generous than the ones they paid their parents, and likely more generous than those to be received by their children.

Prior to the baby boomers reaching retirement, pensioners were the group most associated with poverty. But between 1995 and 2010 pensioner incomes doubled in real terms and since then, they have stabilised at that new higher level.

That’s partly because of the state pension, which now pays out vastly more than it did in previous generations, when measured as a proportion of median earnings.

Some of today’s pensioners still receive money from the State Earnings Related Pension Scheme, a very generous programme that accepted new entrants from 1978 until 2002. It was scrapped as it was deemed unaffordable. Then of course, most receive a basic state pension – which has been bolstered since the early 2010s by the triple lock (a policy that cost far more than ever imagined).

But the other, and perhaps greatest piece of luck was that my generation worked in an era in which employers – public and private – offered membership of defined benefit pension schemes. That meant that through one’s career, we earned entitlements to a decent pension set at a fixed proportion of salary.

Getty Images

Getty ImagesThose schemes became expensive for employers to sustain as life expectancy improved, and they all but died out in the private sector in the 2000s.

Instead, most millennial and Gen Z employees now accumulate savings in a personal pension pot, which is invested and pays out whatever is in the fund. They may be lucky with the amount they earn on their savings; they may be unlucky.

But the really striking thing is just how much employers have been putting into each type of pension. Looking back at ONS data, you’ll see that for the defined benefit pension – the “guaranteed” scheme enjoyed by some boomers – the typical private sector employer contributes 15% to 20% of salary every year. It’s a substantial cost, and explains why employers withdrew them. For the defined contribution pensions – the ones hoisted on millennials – the private sector employer typically pays in 3% of salary. That is quite a difference.

All in all, it is understandable if my younger colleagues feel aggrieved.

Again however, we also need to acknowledge that many people of my generation didn’t have a defined benefit pension. In 1997, before the mass closure of such schemes in the private sector, they were still (just) a minority luxury.

Spluttering growth

I think it’s clear I was particularly lucky.

I went to university before I had to pay, I bought a flat in London in 1988 and I worked for an employer that offered me a generous defined benefit pension.

But you mustn’t confuse the luckiness of some within the late baby boom, with the luckiness of the whole cohort.

So rather than saying that late baby boomers were a lucky generation, I’d suggest the late baby boom was a particularly great generation in which to be lucky.

But there is one other factor at play.

Arguably, the grand disappointment of the last two decades has not been the cost of higher education, pensions or even housing; it has been the decline in per capita economic growth that occurred around the time of the great financial crash in 2007/08.

Put simply, the country is not as rich as it would like it to be: year by year, wages don’t grow as fast as we’d expect; taxes have to be higher to pay for things; imports are more expensive to buy. The lack of economic growth surely accounts for a shared sense of material deprivation.

Getty Images

Getty ImagesBroadly speaking, if the economy grows at a per capita rate of 2% a year, which we regarded as normal in the 1980s and 90s, then every fifteen years, average incomes grow by about a third. Each cohort is comfortably richer than the one before.

But when per capita incomes grow at an average of 1% a year, which is closer to the experience this century, average incomes only grow by about 16% over a 15-year period. That’s not enough to ensure that all age groups are richer than their predecessors.

Even though the baby boomers are not the richest of cohorts, some of us have been blessed to have lived and worked in a country that seemed to be on a growth trajectory – things were getting better. It’s odd to say, but I’d wager that most of us would rather live in a poor country where things are improving, than a richer one where everything seems to be in decline.

To end arguments about intergenerational equity, we need to work out how to restart the growth engine that has been spluttering.

Top image credit: Getty

BBC InDepth is the home on the website and app for the best analysis, with fresh perspectives that challenge assumptions and deep reporting on the biggest issues of the day. Emma Barnett and John Simpson bring their pick of the most thought-provoking deep reads and analysis, every Saturday. Sign up for the newsletter here